Millennials Are More Likely to Buy Their First Homes in Cities

Millennials Are More Likely to Buy Their First Homes in Cities

If there’s a single question that has gnawed at urban economists and planners over the past few years, it’s this: Will Millennials’ well-known love of cities fade once they have kids and need space for double strollers and play kitchens, or is it a more lasting shift in how Americans will decide where to live? We’ve heard the argument that Millennials have “peaked” in cities and will eventually suburbanize from demographer Dowell Myers (cited by Conor Dougherty in the New York Times), and the counter-argument from City Observatory’s Joe Cortright and others. One researcher, Harvard’s Hyojung Lee, has tried to square the circle by arguing that Millennials are both urban and suburban.

Although it doesn’t put the debate to rest, a new paper shows that Millennials are at least continuing to tilt urban as they stop renting and become homeowners.

The paper, published in the Journal of Planning Education and Research, looks at whether Millennial first-time homebuyers (defined as those born between 1980 and 2000) are more likely to buy homes near city centers than their counterparts in Generation X. Authors Elora Raymond of Clemson University, Jessica Dill of the Federal Reserve Bank of Atlanta, and Yongsung Lee of Georgia Institute of Technology used a logistic regression model controlling for age and generation; they also controlled for income, credit score, car ownership, mortgage size, mortgage payment, and student-debt level. The upshot: The odds of Millennials buying near city centers are 21 percent higher than for Generation X.

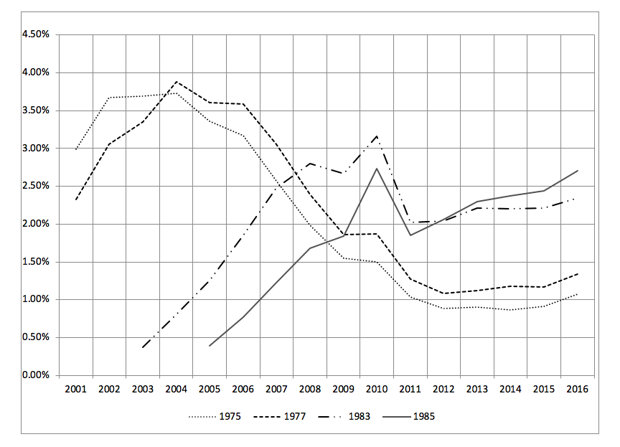

The study’s dataset was a random sample of more than 100,000 personal credit records from 2001 to 2016. Out of that, the researchers selected people who took out mortgages for the first time, then narrowed that subset to first-time buyers within a 10-mile radius of the country’s 50 biggest Metropolitan Statistical Areas. “It’s a random sample of a very large slice of the population, and it’s truly random,” said Raymond. Collecting 15 years of data let the authors compare Gen Xers and Millennials buying first homes at the same ages—but also at different ages.

Interestingly, despite all we’ve read about ballooning student-loan debt and stagnant incomes, Millennials buying homes for the first time had a higher median credit score than their older counterparts for most of the study period. The median age of first-time homebuyers actually went down slightly year on year from the peak of the housing boom—from 35 in 2001 to 33 in 2014. Credit tightened more for older buyers than for younger buyers after the crash, possibly because it had loosened more for them during the boom. That “may explain why first-time home purchases have fallen faster for older buyers than younger buyers,” the authors write.

First-time home purchases by birth cohort

A strong credit score and high income had “a small but significant relationship” with the purchase of a close-in home. But the factors that really influenced whether a first-time buyer moved within 1 mile of a city center were not financial. They were age (younger adults are more likely to live near city centers, irrespective of generation); being a member of the Millennial generation; and not owning a car. The effect of owning a car or two on not living downtown was striking:

The number of cars sharply reduced the odds of buying one’s first home in a city center. Owning one car corresponded with 21 percent lower odds, and those who owned two cars had 41 percent lower odds of purchasing homes in city centers.

The policy implications are, in short, that the U.S. must plan for higher densities and non-car mobility if the back-to-the-city movement is not a blip.

Raymond acknowledged it’s possible that even if Millennials buy their first homes in the city, they could still go on to buy their second (and third) homes in more distant locations after that. Perhaps a starter condo comes before the leap to a suburban Cape Cod. But the finding about first homes is significant regardless, she said.

“The main point is: Their first home is closer to downtown or more likely to be right downtown than a Gen Xer’s first home. A lot of people have said, ‘Millennials are just renting downtown.’ That’s what this paper shows is not true.”

About the Author

Source: https://www.citylab.com/life/2018/11/millennials-buy-homes-cities-generation-x-suburbs/575755/\